Electronic Shelf Label Market 2026: Size, Trends, and What Buyers Need to Know

The electronic shelf label market is at an inflection point. After years of early adopters and pilot programs, 2026 marks the year ESLs shift from a retail novelty to an operational necessity — driven by Walmart-scale RFID rollouts, the arrival of an open Bluetooth standard, and AI-powered dynamic pricing moving from concept to production. But for procurement teams and retail operators evaluating whether now is the right time to invest, the market research reports only tell half the story.

This article covers the numbers you need, the technology choices that matter, and — more importantly — the barriers most market reports skip.

How Big Is the Electronic Shelf Label Market in 2026?

Pick up five market research reports and you will get five different numbers. The reason is simple: each firm counts a different slice of the market. Some track hardware only. Others bundle software licenses, installation, and maintenance contracts. But the picture they collectively paint is consistent: this market is large and accelerating.

| Year | Market Size (USD) | Source |

|---|---|---|

| 2025 | $2.2–2.66 Billion | GM Insights, Fortune Business Insights |

| 2026 | ~$3.0 Billion | Fortune Business Insights |

| 2030 | $3.8 Billion | Mordor Intelligence |

| 2034–2035 | $7.4–8.45 Billion | GM Insights, Fortune Business Insights |

The compound annual growth rate lands consistently between 12% and 17%, depending on which forecast period and methodology you trust (Fortune Business Insights, 2026; Global Market Insights, 2026). To put that in perspective: by 2035, the global ESL market will be roughly the size of a small nation’s economy — a country’s worth of digital price tags.

Europe remains the largest regional market, holding roughly 38–48% of global ESL deployments, valued at $553 million in 2025 alone. Asia-Pacific is the fastest-growing region at a 13.6% CAGR, driven by retail modernization across China, India, and Japan. North America commands about 31% of the market, with the U.S. alone accounting for an estimated $609 million in 2025.

The takeaway for buyers: the market is big enough that supply chains are mature, but fragmented enough that you still have negotiating power. More on that in the vendor section.

What’s Driving the Rapid Growth of ESL Adoption?

Three forces are pushing ESLs from “nice to have” to “hard to compete without.”

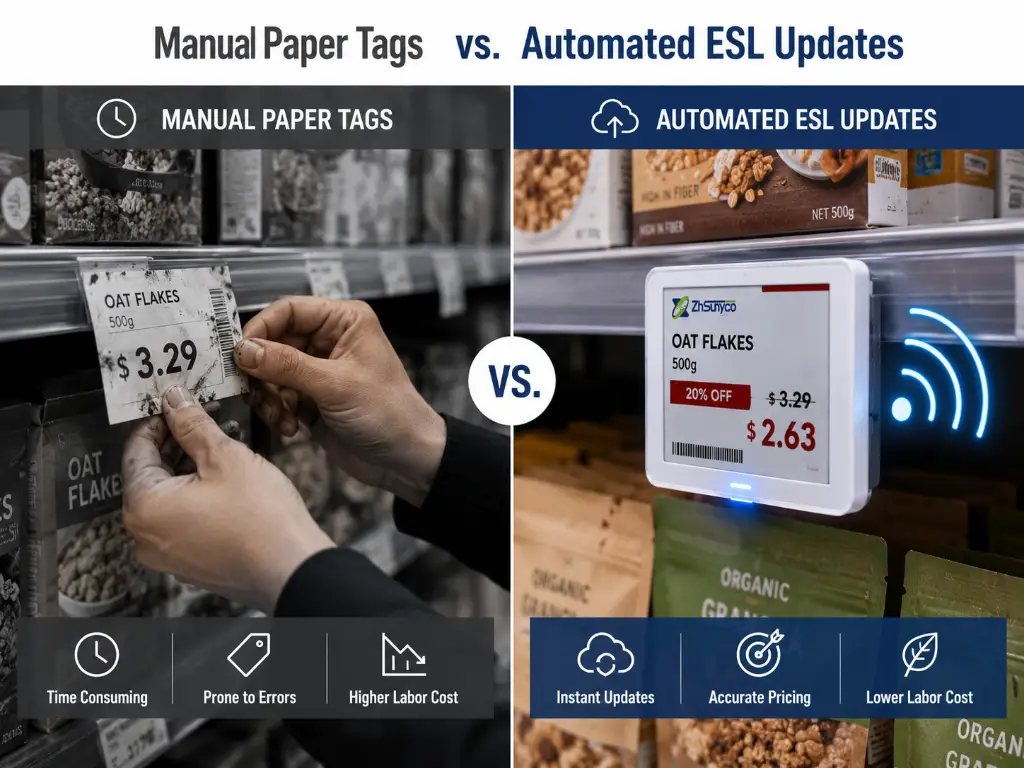

Labor costs are making paper price tags indefensible. A mid-size supermarket spends 15 to 20 staff hours per week on manual price updates — changing tags, verifying accuracy, and fixing the inevitable errors. Paper-based pricing carries a 3–5% error rate, meaning roughly one in every 25 tags on your shelves is wrong at any given moment. ESLs eliminate that labor almost entirely: price changes that took two days now happen in seconds, and error rates drop below 0.1%.

Omnichannel retail is forcing price synchronization. When a customer can check your shelf price against your website while standing in the aisle, a mismatch is not just embarrassing — it is a lost sale or a regulatory liability. ESLs close that gap by making the shelf the same data feed as the e-commerce store, updated in real time across every location.

Sustainability compliance is shifting from voluntary to mandatory. A single supermarket discards 50 to 100 kilograms of paper tags annually. Multiply that across a chain of 50 stores, and the waste — plus the carbon footprint of printing and shipping those tags — becomes a measurable ESG liability. ESLs eliminate that stream entirely, with e-paper displays consuming near-zero power except during the instant of an update.

These drivers explain why the market is growing at double-digit rates. They do not, however, tell you which technology to buy. That requires a closer look.

E-Paper, LCD, or NFC — Which ESL Technology Should You Choose?

Before comparing technologies, ask yourself three questions: What is your store environment (dry retail, cold chain, high-humidity)? What is your budget tolerance per label? And how important is customer-facing interactivity versus pure price display? Your answers will route you to one of two technology camps.

E-Paper ESLs — The Industry Standard for a Reason

E-paper dominates the ESL market, and for good reason. It consumes power only when the display changes — meaning a single battery can last 100,000 refreshes or five to ten years. It is readable in direct sunlight, viewable from wide angles, and thin enough to mount on any shelf edge.

But not all e-paper is the same. The market splits into two tiers:

| Feature | Segmented E-Paper | Full-Graphic E-Paper |

|---|---|---|

| Market share | ~43% | Fastest-growing sub-segment (16.5% CAGR) |

| Display capability | Numbers, text, simple icons | Images, QR codes, logos, multi-language |

| Battery life | 7–10 years | 5–7 years |

| Typical use | Basic price display | Promotional pricing, branding, nutritional info |

| Cost per label | €4–5 | €6–8+ |

Segmented e-paper is the workhorse. If your priority is replacing paper tags with something that shows prices accurately and runs for a decade without a battery swap, this is your default. Full-graphic e-paper is the marketer’s tool — capable of displaying product images, promotional QR codes, and allergen warnings alongside the price. The four-color e-paper panels (black, white, red, yellow) that reached commercial maturity in 2024 add a visual dimension that segmented screens cannot match.

The choice logic: if your stores compete on price and efficiency, segmented e-paper gets the job done at the lowest total cost. If visual merchandising drives your sales — specialty retail, premium grocery, pharmacy with regulatory labeling — the full-graphic premium pays for itself in customer experience and promotional flexibility.

LCD and NFC-Enabled ESLs — When You Need More Than E-Paper

LCD shelf-edge displays are the vibrant cousin in the ESL family. Using BOE, LG, or Samsung panels with 2K resolution, they deliver full-motion color that e-paper cannot match — ideal for fresh produce sections, promotional end caps, and high-traffic zones where visual impact drives impulse purchases. The trade-off is power consumption: LCD panels draw continuous current and have a rated lifespan of 50,000 hours (roughly five to six years of continuous operation), compared to e-paper’s near-decade on a single battery.

NFC-enabled ESLs add a different layer entirely. With a 19.5% CAGR, NFC is the fastest-growing communication protocol in the ESL space — not because it replaces e-paper or LCD, but because it adds a consumer interaction layer on top of either display technology. A shopper taps their phone against an NFC-enabled price tag and instantly sees product origin, allergen details, loyalty points, or a promotional video. For pharmacy chains needing to display regulatory information without cluttering the shelf, or for apparel retailers wanting to bridge the physical-to-digital gap, NFC turns a price tag into a customer engagement endpoint.

Think of it this way: e-paper is the e-reader — efficient, readable, built for one job. LCD is the tablet — dynamic, colorful, power-hungry. NFC is the tap-to-pay chip — it does not replace the screen; it adds an interaction layer on top of whatever screen you choose.

Who’s Who in the ESL Market — Key Players and Competitive Dynamics

The ESL market is fragmented, which is good news for buyers. The top five players collectively hold only 34.8% market share — meaning nearly two-thirds of the market belongs to smaller, often more specialized vendors.

Tier 1 — The Giants. VusionGroup (formerly SES-imagotag) leads with approximately 18.1% global share, boosted by its acquisition by BOE Technology — a move that vertically integrated the world’s largest e-paper display manufacturer with the largest ESL solutions provider. Pricer AB, a Swedish pioneer in optical wireless ESL, dominates European grocery. SOLUM, backed by Samsung’s manufacturing scale, is the strongest Asia-based contender expanding aggressively into Western markets.

Tier 2 — The Challengers. Hanshow Technology has differentiated through AI — its NexShelf platform, unveiled at NRF 2026, introduced centimeter-level Store Digital Twin technology with 95%+ accuracy in mapping real shelf conditions. E Ink Holdings is not an ESL vendor per se, but supplies the e-paper displays inside most of the world’s ESL tags — making them a critical upstream player. Displaydata (now folded into VusionGroup) pioneered cloud-managed ESL architectures.

The choice framework for buyers: market share does not equal suitability. A vendor with 18% global share may be optimized for 500-store supermarket chains and offer a poor fit for your 30-store pharmacy network. Evaluate on three dimensions: protocol openness (can you switch vendors without replacing hardware?), software ecosystem (does it integrate with your POS/ERP, or does it demand you adapt to theirs?), and local support (does the vendor have regional warehouses and technical teams, or will a hardware failure mean shipping tags back to Asia?).

-

Protocol openness — Can you switch vendors without replacing hardware?

-

Software ecosystem — Does it integrate with your POS/ERP?

-

Local support — Regional warehouses and technical teams, or shipping back to Asia?

The ESL market today looks a lot like the smartphone market in 2012 — there are clear leaders, but the game is far from over, and the fragmentation means buyers who do their homework can negotiate from a position of strength.

The Real Barriers — What Most Market Reports Won’t Tell You

Here is what the 15% CAGR charts do not show: for every retailer who successfully deploys ESLs across their chain, there is another who spent six figures on a pilot that never scaled.

Beyond the Price Tag — The True Cost of ESL Deployment

The number you will hear first is €5 to €6 per label. That is the hardware unit cost for a standard black-and-white e-paper tag. It is also the smallest line item on your actual invoice.

For a mid-size supermarket with roughly 10,000 SKUs, the visible costs are the tags themselves: approximately €50,000 to €60,000. The invisible costs are where budgets blow out. Base stations and access points — the wireless infrastructure that communicates with every tag — add 15–25% on top of the tag hardware, and the number of access points scales with store square footage and shelf density, not SKU count. Software licensing comes in two models: one-time perpetual fees or annual SaaS subscriptions, and the total cost difference between the two can exceed 40% over a five-year window. Installation labor, staff training, and the first year of maintenance support typically add another 10–15%.

Then come the environmental variables. Standard e-paper tags are rated for 0°C to 50°C. If your stores have freezer aisles (−25°C) or high-humidity fresh-produce sections, you need specialized tags that cost 1.5 to 3 times the standard unit price — and their batteries degrade in three years instead of five.

All in, a 10,000-SKU deployment realistically lands between €85,000 and €120,000 in total three-year cost of ownership. The vendors who quote an 18-to-24-month payback are basing that math on one assumption above all others: that your largest cost saving comes from labor reduction. If your stores operate in a region with low hourly wages, or if your labor contracts make headcount reduction difficult, that payback timeline stretches — and in some cases, disappears.

The ROI question is not “do ESLs pay back?” It is “does YOUR store’s labor profile, error rate, and promotional frequency generate enough savings to clear YOUR cost of capital within a timeline YOUR board will accept?” If you cannot answer that with your own numbers, no vendor’s ROI calculator will answer it for you.

Integration Headaches and Vendor Lock-In — The Hidden Risks

In 2025, New Zealand’s Woolworths had to close all 185 of its stores for a full day because of an ESL pricing error. The tags displayed prices that did not match the point-of-sale system — and under New Zealand consumer law, the shelf price is the legally binding price. One software glitch, 185 stores dark, a national news cycle of customer outrage.

The Woolworths incident is extreme, but the underlying vulnerability is universal. When you deploy ESLs, you are grafting a new system onto an existing organism that already has a brain (your POS), a circulatory system (your inventory database), and decades of scar tissue from legacy ERP integrations. If those systems do not talk to each other cleanly, the ESLs will display the wrong price with the same speed and precision they were designed to display the right one.

Then there is the lock-in problem. Most ESL systems on the market today use proprietary wireless protocols — typically a vendor-specific implementation of 2.4 GHz or 433 MHz. That means the tags from Vendor A cannot talk to the base stations from Vendor B. If you deploy 10,000 tags on a proprietary protocol and later decide you want to switch vendors, you are not switching software — you are replacing every piece of hardware in every store. The switching cost is effectively the original deployment cost, paid again.

This is not an argument against ESLs. It is an argument for doing vendor due diligence on protocol openness before you sign. The Bluetooth SIG published an open ESL standard in 2024, and the first Bluetooth-standards-compliant products are expected to reach commercial maturity in 2026–2027. That standard does not solve every interoperability challenge, but it gives buyers a credible alternative to proprietary lock-in.

When evaluating vendors, ask three questions: Does the system support open protocols (MQTT, Bluetooth standard) or only proprietary ones? Is the software available as a one-time license with local deployment, or is it SaaS-only with mandatory cloud dependency? And what is the hardware warranty policy — repair-and-return, or replacement-only?

Some manufacturers have built their systems specifically to address these concerns — offering MQTT-open base stations that integrate with existing POS and IoT infrastructure, one-time software licensing with free lifetime updates and optional on-premise deployment, and a replacement-only hardware warranty that keeps failed tags out of repair limbo. The difference between a vendor who locks you in and one who gives you an exit path is not always visible on the spec sheet — but it will determine whether your ESL deployment is an asset or a liability three years from now.

Where the ESL Market Is Headed — 2026 and Beyond

Three developments will reshape the ESL market over the next two to three years, and none of them are incremental.

AI turns the price tag into a pricing engine. ESLs have always been output devices — they display the price someone else decided. With AI-driven dynamic pricing, they are becoming input devices that feed shelf conditions, sales velocity, and competitor data into algorithms that set prices autonomously. Hanshow’s NexShelf platform demonstrated centimeter-level product detection at NRF 2026 — the shelf knows what is on it, what is missing, and what is selling, without manual scanning. Early adopters report up to 15% reduction in food waste through automated expiry-based markdowns, and 10–15% improvement in inventory turnover through demand-responsive pricing.

RFID + ESL fusion makes every item individually trackable. Walmart’s 2,300-store RFID rollout in 2026 — covering meat, bakery, and deli — is the largest single-item-level tracking deployment in retail history. When every product has a unique digital identity and every shelf has a connected display, the boundary between “inventory system” and “pricing system” dissolves. A tag on a shelf does not just show a price — it knows exactly which batch of products is in front of it, when they expire, and whether any have been misplaced.

Bluetooth standardization breaks the proprietary wall. The Bluetooth SIG ESL standard, published in 2024, is the first genuine industry attempt at interoperability. If it achieves broad adoption — and early signals from component manufacturers suggest it will — the lock-in argument against ESL adoption evaporates. For mid-size retailers who have been waiting on the sidelines, a standards-based ESL market in 2027–2028 could be the catalyst that turns “we’re watching the space” into “we’re issuing an RFP.”

The ESL market in 2026 is not just growing — it is becoming structurally more accessible. Standardization lowers switching costs. AI makes the ROI case stronger. RFID integration makes the value proposition broader than labor savings alone. For procurement teams who do their homework on total cost, protocol openness, and integration complexity, the window to deploy ahead of competitors is open. It will not stay open forever.